On April 6th 2021 the rules for IR35 in the private sector will change and it’s important that both contractors and the end-clients who employ contractors take action.

Since April 2000, the Intermediaries Legislation, more commonly known as IR35, has been used by HMRC to combat tax avoidance by so-called “disguised employees” that operate as contractors for businesses.

IR35 will extend its reach from April 2021, when further changes are applied to the private sector as the government continues to crack down on perceived tax avoidance through intermediaries.

What are the key changes being implemented?

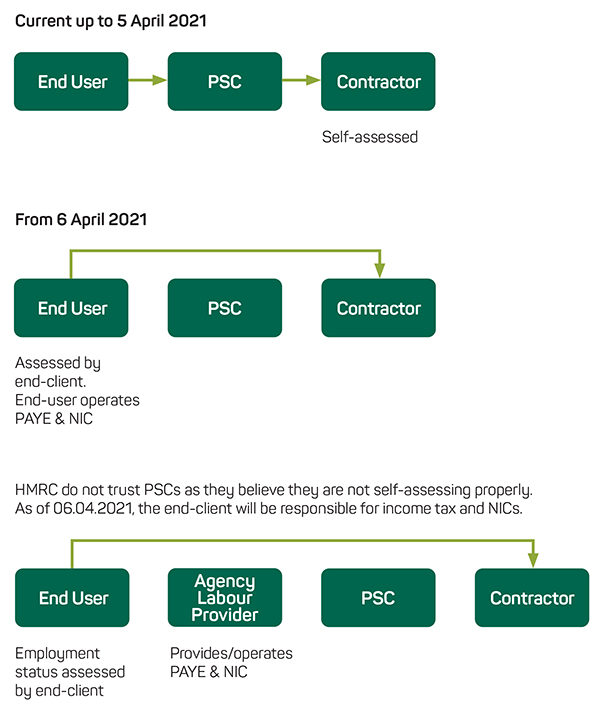

At present, the onus is on the contractor to determine his/her employment status and the correct level of tax they should pay.

From April, the responsibility for determining IR35 status will sit with the end-client. This means that any unpaid tax can be collected from both parties if an error has been made.

If a contractor is suspected to be working inside IR35 when they have claimed they are working outside IR35, then they should prepare to be investigated by HMRC.

A tax enquiry investigation such as this can be backdated up to six years, and any owed tax from that period will be claimed back by the government.

Due to these changes to the legislation, it has become imperative that contractors have their contracts reviewed so any necessary amendments can be made with their end-client.

Call 0333 321 1403 for details about IR35 contract reviews.

Which employers will be affected by the private sector IR35 rollout?

It was announced in the 2018 budget that IR35 would be extended to the private sector from April 6th 2020, with the exception of small organisations. The date was extended to April 6th 2021 due to the Coronavirus.

The definition of a ‘small organisation’ is similar to that defined in the Companies Act 2006.

A small company must not meet two of the following criteria:

- Net turnover exceeding £10.2m

- Balance sheet totalling more than £5.1m

- More than 50 employees

The reform is expected to impact most private sector contractors, the majority of whom work for large companies, such as banks and other financial organisations and the construction sector.

The private sector rollout is predicted to net the Treasury an additional £1.3bn per year in tax revenue from 2023. So, if anyone is still harbouring any hope that private sector IR35 will be scrapped they are going to be disappointed because this tax revenue is needed to help balance the UK’s books.

What can we expect from the IR35 new rules?

The private sector rollout of IR35 could lead to a significant loss of earnings for private sector limited company contractors who find themselves working inside IR35.

What is also expected is a significant contraction in the number of freelance contractors who work for their own limited company. This is due to them opting for working for an Umbrella company, or simply closing their limited company altogether and returning to the full-time workforce.

However, it is important to remember that contractors will still be required and paid a premium for their specialist skills in comparison to what regular employees are paid.

Whatever happens, it has never been more important for both the contractor and the employer/end-client to know exactly where they stand and to take action to remedy any potential future issues.

Can I insure against IR35?

There are measures contractors can take to mitigate the potential fallout from the private sector IR35 rules.

Contractors should always make sure they are adequately insured. If you’re a freelance contractor, then you will undoubtedly hold both professional indemnity insurance and public liability insurance as these two insurance policies are often stipulated in contracts before the work is awarded.

At Caunce O’Hara we also offer a range of insurance products that are more specific to IR35 legislation, including:

Legal Expenses Insurance

Caunce O’Hara’s Legal Expenses Insurance provides you with £100,000 of cover, in any one claim, for legal representation costs incurred in the event of an IR35 investigation against you.

The policy is split into two tiers. Tier 1 being the core cover the policy provides, and Tier 2 being the extra cover that is available to you.

The policy provides cover for the following:

- Employment disputes

- Employment compensation awards

- Property and landlord and tenant disputes

- Criminal defence

- Tax protection

- Regulatory compliance

- Court attendance costs including jury service

- Employment extra protection

- Identity theft

- Contract disputes

IR35 Contract Review

Contract Reviews are available for only £60.00 per contract when purchased with the Legal Expenses Insurance policy. The contract review will look at both the specific contract signed by the contractor and the working practices of the contract. The review will be undertaken by an IR35 Contract Reviewer whose procedures have been approved by our partners. The review must pass the contract/engagement as being outside IR35, and not caught by the IR35 Intermediaries Legislation.

This same review service also applies to a Statement of Work. If you would like a SoW reviewed call our team on 0333 321 1403

Tax Losses Insurance

Based on the result of the IR35 Contract Review determining the contractor to be working outside IR35, this policy will cover the net tax loss, which arises when HMRC successfully argue that an Insured’s Qualifying Contract falls within the scope of IR35. The contract review must “pass” the contract/engagement as being outside IR35 before the Tax Losses Insurance policy will be made available to purchase.

Professional Expenses Insurance

PEI is an insurance policy, which must be taken out with the Tax Losses Insurance policy, that ensures a HMRC IR35 investigation can be professionally defended by extending the notification period.

The notification period is the period of insurance during which the insured person is entitled to make a claim plus any extension by virtue of the Professional Expenses Insurance and the renewal of the Professional Expenses Insurance, which is taken out with the Tax Losses policy.

The insured person must continue to renew their PEI even when not undertaking any contracts otherwise they will invalidate the Tax Losses Insurance policy.

For further information about IR35 Insurance please contact our award-winning team on 0333 321 1403

Disclaimer:

This material is intended for general information purposes only and does not constitute legal advice. Specialist legal advice should be taken in relation to specific circumstances.

Doanload the Fee-payers’ IR35 Guide here