Regardless of the industry you operate in, if you are a contractor or freelancer working under a limited company, IR35 legislation could affect you. To avoid tax and National Insurance liabilities and potential penalties, it is important that you understand IR35 and what actions you need to take to remain compliant.

Explore our guidance below, created in collaboration with Markel Tax, to help you understand IR35.

What is IR35?

IR35, also known as off-payroll working rules, was passed in 1999. The legislation was then introduced in the Finance Act of 2000 by the government under Chapter 8 Part 2 ITEPA 2003, aimed at individuals who were disguising themselves as independent contractors, resulting in most cases paying lower rates of tax and NIC, when in fact their relationship with their clients was more akin to an employment relationship. The name itself was coined from the press release reference (Inland Revenue 35) issued by the Inland Revenue before it became known as Her Majesty’s Revenue & Customs (HMRC).

The Intermediaries Legislation was created to ensure that workers operating through a limited company and end-clients pay the right amount of employment taxes, with the intention of eliminating any differences between employed workers and self-employed contractors carrying out similar work.

Your IR35 status affects how much tax and National Insurance you pay if you contract through your own limited company. If you are subject to IR35 then PAYE and both primary and secondary Class 1 National Insurance Contributions (NICs) will be due – this means a higher tax bill and less take-home pay.

IR35 aims to improve tax fairness, so that those contractors who are being treated as employees broadly pay the same amount of tax as employees.

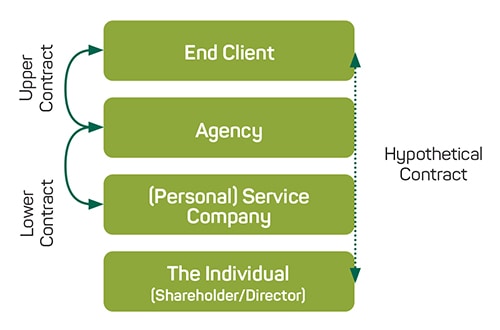

A typical example of a contractual chain:

What is IR35 status decided by?

From April 2021 new tax legislation was introduced, Chapter 10 Part 2 ITEPA 2003. This transferred the responsibility for deciding IR35 status to the end-client if it was deemed a medium or large sized business and operating within the private sector. For end-clients in the public sector this responsibility automatically applies, regardless of size, and has been in place since April 2017.

The tax and NIC liabilities for getting IR35 wrong also shifted from the contractor to the entity that pays the contractor’s limited company (the fee payer), typically a recruitment agency although this could also be an end-client for direct contractual engagements.

Before April 2021, it had always been the responsibility of contractors to determine whether the relationship with their end-client is genuinely one of self-employment or disguised employment. This is still the case where the private sector client is a small business and exempt by the Chapter 10 legislation from making any IR35 status decisions, or where the end client is wholly overseas with no link or permanent establishment in the UK.

One of the main reasons the government decided to introduce the new off-payroll working rules was due to the increasing number of individuals that were working though a limited company and the lack of resource available to HMRC to effectively police the IR35 legislation. By making end-clients, in most cases, responsible for deciding IR35 status, HMRC have stated that compliance has significantly increased, although many would argue that many contractors that genuinely operated outside of IR35 have become collateral damage due to end-clients not wanting to engage with the Chapter 10 legislation because of the associated risks involved.

Who does IR35 apply to?

IR35 status is determined by your contractual terms and conditions and your working practices in the context of case law precedent, judgements that are handed down by the courts and tribunals which give key indicators as to whether someone is employed of self-employed.

If you feel unsure of whether you fall inside or outside IR35, seeking professional advice may help to put your mind at ease. A contract review service will provide you with a clear explanation of your status in the eyes of HMRC and will help to clarify whether you fall inside or outside IR35.

During the review, the clauses in your contract will be checked for compliance and to verify whether your working practices follow the terms and conditions outlined in your contract.

You can check your IR35 status via the HMRC Check of Employment Status Tool (CEST).

What does inside IR35 mean?

If, as an independent contractor, you are deemed to be working inside IR35, then you are deemed as a disguised employee. This means you must pay broadly the same taxes and NIC as an employee, without being afforded the rights or benefits associated with employment.

What does outside IR35 mean?

Being outside IR35 means you are operating as a genuine business, and not as a disguised employee of your end-client. Any income generated from your contracts will be paid gross without any tax and NIC deductions. This means you are able structure how you pay yourself from your limited company and remain responsible for paying your own taxes and national insurance contributions.

What happens if the rules apply?

You will need to consider IR35 rules before taking on any new contract, and identify whether it is the responsibility of your end-client to decide your IR35 status or whether that decision remains with you. Where the IR35 status decision rests with your end-client, they must issue you with a Status Determination Statement (SDS) setting out their IR35 opinion and the reasoning behind such.

If IR35 applies to your contract, you can also consider the following options:

- Advise your end-client at the earliest opportunity that you want to challenge their IR35 decision through their disagreement process, which they must provide and respond to your contentions and supporting evidence within 45 days of receipt of your disagreement.

- Decline the contract and seek work which is not subject to IR35.

- Explore whether it is possible to work as an employee rather than a contractor. While you would pay tax and NICs as an employee, the benefit would be that you would be entitled to the rights and protections of an employee.

- Opt to be employed by an umbrella company and entitled to employee benefits such as holiday pay, sick pay and ‘continuous employment’, which is helpful when securing mortgages and other loans.

Working through an umbrella company

A compliant umbrella company will provide you with full-time employment rights such as holiday pay, maternity pay, sickness pay, pensions and so on. They will also provide HR functions and the usual employment benefits.

As your employer, the umbrella company is paid by the client you are working for – they will then pay you and deduct any taxes and national insurance. This provides contractors with the stability and advantages of being employed while still also giving them the flexibility to work on contracts with a range of clients.

Discover our knowledge centre for more help and guidance, or read more about Caunce O’Hara’s contractor insurance.

Please note: This article provides guidance for information purposes only. It should not be relied upon wholly when making or taking important business decisions – always seek the services of an appropriately qualified professional. The views expressed by websites referenced to are limited to those of the websites, and do not necessarily reflect the views of Caunce O’Hara. Caunce O’Hara is not affiliated with any of the brands, companies or websites mentioned in this article.