Planning for your future as a freelancer

Posted on 26th July 2021 by Katherine Ducie

As a freelancer you’re fully responsible for planning your future and ensuring you don’t run into any financial difficulties – over the next coming years and further into the future, when you’re retiring. Whether it’s a holiday, parental leave or your retirement, you’ll be relying on the preparations and savings you set in motion now.

That’s why planning for your future is vital. While spending more in the moment can be tempting, prioritising your savings and making preparations instead will pay huge dividends in the future.

In this article, we will discuss how you can plan for your future in the long term as well as in the nearer future for holidays, sickness, tax bills and other expenses.

Life insurance

Life insurance for freelancers can be a good alternative to the standard employee ‘death in service’ benefits that permanent employees are provided with.

Holding a life insurance policy means that if anything happens to you, your spouse or family are given a financial pay out to safeguard their future. If your family for example has a mortgage and you’re the breadwinner, this type of insurance can help cover these kinds of payments and ease financial worries.

Another option to consider that varies slightly from Life Insurance is Relevant Life Insurance. Instead of taking the policy out yourself, it is taken out by your limited company on behalf of yourself or an employee.

This can be a favorable option for contractors and freelancers, as it’s considered to be a more tax efficient option. This is because the premiums will not be paid from your personal post-taxed income and are instead paid by your limited company. Premiums for relevant life insurance can be claimed as a business expense, as long as you can show that they are legitimately for the purposes of the business.

It’s worth noting that if you write your policy into a trust, the payout will not form part of your estate. This means that your family will not have to go through the long probate process to receive the funds.

Pension

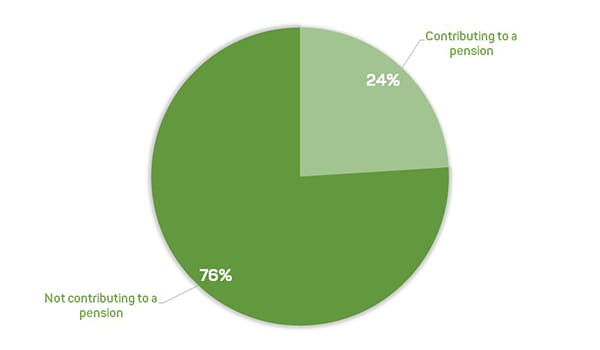

A survey by National Employment Savings Trust (NEST) revealed that only 24% of self-employed people currently contribute to a pension. The research which surveyed 2,000 self-employed individuals also showed that 35% of these individuals are ‘put off thinking about pensions because it makes them feel nervous’ (2).

For the self-employed, knowing the best option to take with a pension isn’t easy and sometimes the right guidance can be difficult to find. If you’re not currently saving towards a pension, focus on saving what you can, when you can to begin with. Try and put something towards your pensions regularly, even if it’s a small amount. It all adds up.

Break it down into a daily saving rate that sounds achievable – for example £3.30 a day, which amounts to roughly £100 a month.

You might want to save for your pension in other ways such as by saving into an instant access savings account specifically for retirement or by saving into a cash ISA so that you can access your money more easily however if you decide to save up through a traditional pension, you can benefit from government top ups to your pension.

Think of your pension as a tax-free way to save for your retirement. You can obtain tax relief on private pension contributions worth up to 100% of your annual earnings (3), whereas with ISA’s you won’t receive this tax relief.

Some practical ways to save for your pension, suggested by NEST, include:

- Setting a monthly amount

- Setting an income percent monthly

- Setting an amount from profit yearly

- Setting an income percent yearly

- Left over funds automatically swept up

- Setting a percent of invoices charged

When it comes to choosing your pension, there are various options to choose from including:

- A government-backed pension with Nest

- A personal pension scheme

- A self-invested personal pension

With a nest pension, they’ll automatically claim basic rate tax relief on any contributions you pay into your account. For higher-rate taxpayers, you can claim extra through your tax return. Through this scheme you can pay as little as £10 per contribution and save up to £40,000 in total per year.

Having a pension does usually come with a charge, however they are usually relatively low. Before choosing a pension that’s right for you, it’s always best to do your research and read the terms and conditions before signing up.

To help work out your retirement income and for tips on how you could increase it, you could use a tool like the GOV.UK’s pension calculator.

Protecting yourself from claims after you’ve closed your business

When it comes to your retirement and the time where you decide to close your business, you might want to consider purchasing professional indemnity run off cover.

This is because, even if your business is no longer trading, you could still have a claim made against you, for example a negligence claim made by an old client. These kinds of claims can be made against you for up to 6 years after you’ve closed your business.

Professional indemnity insurance is provided on a ‘claims made’ basis. This means the PI insurance policy must be in force at the time a claim is made for it to cover your business, regardless of when the work was undertaken.

This cover is usually a fraction of the premium of full PI insurance and in some cases, the premium may decrease year on year.

Once you’re happily retired, the last thing you’ll want is a historic project causing problems for you, in the form of a professional indemnity claim, which is why professional indemnity run off cover can be of value.

Savings for the short term

Now that we’ve covered planning for the long-term future, it’s worth having a think about the short-term future too. As you’ve likely experienced, freelance and contractor work can be feast or famine. At times, you’ll have to turn clients away or recommend another freelancer while during other months you haven’t got enough work to fill the week, never mind the month. This has been felt more than ever by many freelancers during the COVID-19 pandemic.

Saving all year round, especially during the months where you have a lot of work on, will help cover your bills during the quieter months.

Other things you need to save for to cover the year ahead are:

- Holidays

- Sick days

- Appointments and family commitments

- Tax bills

Martin Lewis, founder of MoneySavingExpert.com, suggests setting up an emergency fund of around six months’ worth of bills (4). For anyone who feels this would be hard to achieve, Lewis added that saving three months’ worth of bills is ok. Aim for the value you feel is within your reach.

Saving for some freelancers can feel impossible. It’s easy to recommend but extremely difficult to do when you have a lot of outgoings to pay for. Everyone’s circumstances are unique; you might be a single parent who between paying for your monthly food shop, kids birthday presents, after school hobbies and family days out, has no spare cash left at the end of the month. Other freelancers simply might be working in a field where making a lot of profit can be difficult or may be new to freelancing.

If you feel this way, just do the best you can. Paying your bills is more of a priority than saving but saving something, no matter how small, is still worthwhile. Try not to overface yourself with a monthly savings target that is impractical. Be realistic, even if it’s simply putting away what you have saved from buying fewer takeaway coffees over the month. You’ll be surprised by how quickly small contributions can add up.

Holidays and time off

As a freelancer, you don’t get paid for the time you have off, so you need to spread out your profit to make sure it covers the days where you’re not working.

A study by IPSE discovered that only 2 in 5 freelancers financially prepare for taking time off (1). This includes setting money aside for holidays as well as budgeting for lost days of work.

By paying yourself a consistent lower rate, rather than your entire profits during busy periods, it’ll be easier to build up your savings.

Setting aside money throughout the year will stop you having to worry about your finances just before taking time off or overworking and burning yourself out in the weeks leading up to your holiday, to compensate for being off.

Tax bills

In a pot separate to your holiday and time off fund, save up some money each month towards your tax bill. This is really important to avoid being in a position where you have an overwhelming tax bill that you can’t afford.

To help you work out roughly how much you should be setting aside each month, you could use the GOV.UK’s Self-employed ready reckoner. This is designed to help the self-employed budget ahead of their self-assessment tax bill.

Make sure your rates are high enough

Are you charging enough for your services? Without the company benefits you receive as an employee, you need to make sure you’re looking after yourself and giving yourself a good enough chance to prepare for your future.

Not charging enough will make being financially prepared difficult. Therefore it’s crucial to factor your pension, holidays, sick pay, insurances, tax bills and so on into your day rate all year round.

Make sure you are not undercharging and don’t be scared to ask for a little more. Compare your rates with competitors nationally and locally to get an idea of what you might want to charge.

Investing in yourself now can protect you in the future

Protecting yourself with business insurance is another way of protecting your future. Holding insurance like professional indemnity cover can prevent you having to potentially spend your savings on paying out a claim, if one day a difficult client decides to sue you for negligence or breach of confidentiality.

For more information on how you can stay protected with Freelance Insurance, call our friendly team of experts today on 0333 321 1403, or click to get a quick online quote in minutes!

CLICK HERE FOR A QUICK ONLINE BUSINESS INSURANCE QUOTE

Disclaimer:

Please note, this article should not be taken as financial advice.

Caunce O’Hara & Co Ltd and its employees do not provide life insurance policies nor advice regarding life insurance, pensions or accounting.

For financial advice, please consult your accountant or business advisor.

Related articles:

5 ways to reduce your tax bill when self-employed

A guide to freelancer expenses

Dividends and dividend tax rates for the self-employed: what do I need to know?

Sources:

- https://www.ipse.co.uk/policy/research/the-self-employed-landscape/taking-time-off-as-a-freelancer.html

- http://www.nestinsight.org.uk/wp-content/uploads/2019/10/supporting-self-employed-people-save-for-retirement.pdf

- https://www.gov.uk/tax-on-your-private-pension/pension-tax-relief

- https://www.bbc.co.uk/news/magazine-35801951

Sed ut perspiciatis unde omnis iste natus error sit voluptatem accusantium doloremque laudantiumIR35 Hub

Sed ut perspiciatis unde omnis iste natus error sit voluptatem accusantium doloremque laudantiumKnowledge Centre

Sed ut perspiciatis unde omnis iste natus error sit voluptatem accusantium doloremque laudantium